Vietnam, Burundi advance income tax treaty negotiations

Vietnam's Ministry of Foreign Affairs said representatives of Burundi and Vietnam discussed bilateral relations and agreed to direct the relevant authorities to expedite negotiations and the signing of an income tax treaty. The two sides agreed

See More

Vietnam issues comprehensive guidance on the implementation of DTA, MAP, APA

The Vietnamese Ministry of Finance has issued Circular No. 95/2026/TT-BTC, effective from 1 July 2026, setting out comprehensive guidance on the implementation of Double Taxation Agreements (DTAs), Mutual Agreement Procedures (MAP), and Advance

See MoreVietnam issues new regulations on electronic invoices

Vietnam has issued Decree No. 254/2026/NĐ-CP, establishing detailed regulations on electronic invoices and electronic records under the Law on Tax Administration No. 108/2025/QH15. Effective from 1 July 2026, the Decree sets out the framework

See MoreVietnam issues comprehensive tax administration decree with new digital tax, enforcement rules

Vietnam issued Decree No. 252/2026/NĐ-CP on 30 June 2026, providing detailed regulations and measures for implementing the Law on Tax Management. The decree applies to taxpayers, tax administration authorities, tax officials, and other state

See MoreVietnam gazettes decree updating transfer pricing rules

Vietnam has published Decree No. 255/2026/ND-CP, issued on 30 June 2026, introducing a new framework for tax administration of enterprises engaged in related-party transactions. The Decree sets out the principles, methods and compliance requirements

See More

Vietnam extends tax relief on fuel, qualifying raw materials through September 2026

Vietnam’s government has issued a Resolution No. 34/2026/NQ-CP dated 30 June 2026, which outlines the extension of tax incentives for specific energy products. The resolution mandates a continued period of reduced import duties, environmental

See MoreVietnam extends 2026 VAT, CIT, PIT, land rent payment deadlines

Vietnam's government has issued Decree No. 245/2026/ND-CP on 27 June 2026, introducing another round of tax payment deadline extensions for 2026. The measure grants eligible taxpayers additional time to pay value-added tax (VAT), corporate income

See MoreVietnam clarifies CIT incentives for foreign-invested SMEs

Vietnam's Tax Department issued Official Letter 3896/CT-CS, confirming that eligible foreign-invested small and medium-sized enterprises (SMEs) can benefit from a three-year corporate income tax (CIT) exemption under the country's new private sector

See More

Vietnam issues guidance on CbC reporting through automatic exchange of information

Vietnam's General Department of Taxation has issued guidance on the implementation of Country-by-Country Reporting (CbCR) exchange relationships under the Multilateral Competent Authority Agreement on the Exchange of Country-by-Country Reports (CbC

See MoreLiechtenstein, Vietnam finalise income tax treaty negotiations

The Liechtenstein government announced that representatives of Liechtenstein and Vietnam concluded negotiations on an income tax treaty, initialling the agreement on 12 June 2026. The DTA is based on international standards and takes into account

See MoreVietnam clarifies reporting obligations under CbC MCAA

Vietnam's Department of Taxation has released Official Letter No. 3870/CT-CS on 10 June 2026, providing guidance on the implementation of obligations relating to Country-by-Country (CbC) Reports . The guidance follows Vietnam’s accession to the

See More

Albania, Vietnam initial tax treaty following second round of negotiations

Following a second round of negotiations held in Tirana from 2 to 4 June 2026, Albania and Vietnam initialled a tax treaty on 4 June 2026. The two countries signed a memorandum of understanding on the draft treaty. The Vietnamese delegation

See MoreLiechtenstein, Vietnam initial tax treaty after second-round negotiations

Liechtenstein and Vietnam initialled a tax treaty on 12 June 2026 after the second round of negotiations held in Khánh Hòa from 10 to 12 June 2026. The two countries signed a memorandum of understanding. Earlier, officials from Liechtenstein

See More

Luxembourg, Vietnam tax treaty protocol enters into force

The amending protocol to the 1996 income and capital tax treaty between Luxembourg and Vietnam entered into force on 14 April 2026. The agreement seeks to prevent double taxation and fiscal evasion between the two nations. Signed on 4 May

See More

Cyprus, Vietnam first income tax treaty enters into force

The income tax treaty between Cyprus and Vietnam will enter into force on 1 June 2026. Signed on 15 December 2025, it is the first such treaty between the two countries. The Agreement is intended to enhance and expand trade and economic

See MoreVietnam raises tax-exempt threshold for household businesses to VND 1 billion

Vietnam’s Government has issued Decree No. 141/2026/ND-CP on 29 April 2026, introducing amendments and supplements to Decree No. 68/2026/ND-CP on tax policies for household and individual businesses and Decree No. 320/2025/ND-CP guiding the

See More

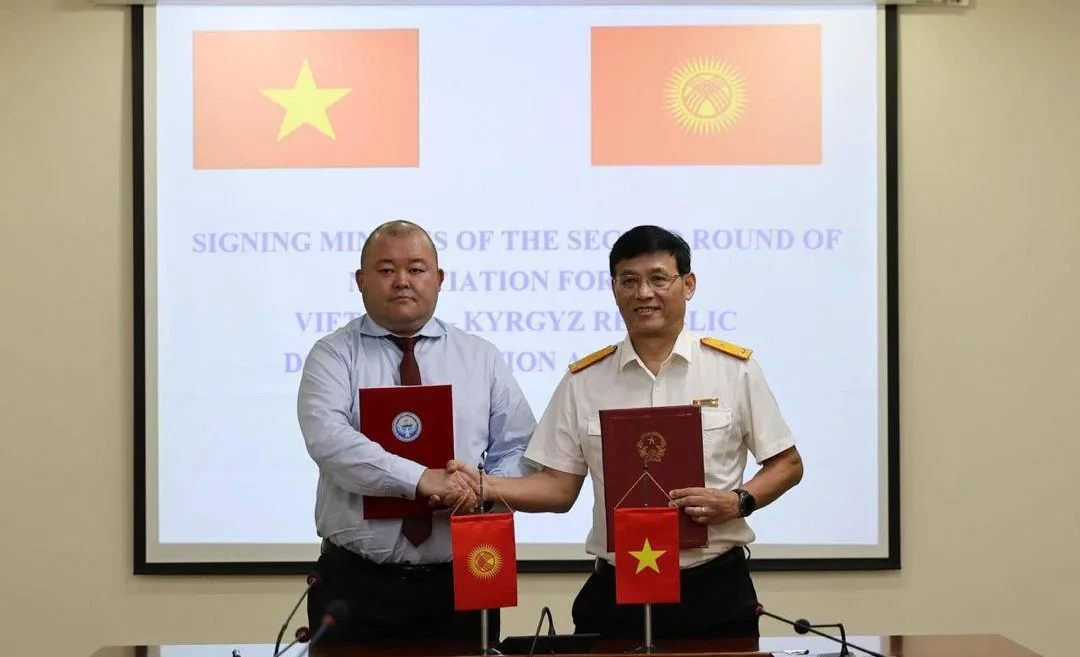

Kyrgyzstan, Vietnam conclude negotiations on income tax treaty

Kyrgyzstan and Vietnam successfully completed negotiations on a draft agreement on the elimination of double taxation, in Hanoi from 21 to 23 April 2026. The Economy Ministry of Kyrgyzstan stated that the agreement will enable entrepreneurs to

See More

China, Vietnam sign customs cooperation agreement

China and Vietnam signed an Agreement on Cooperation and Mutual Administrative Assistance in Customs Matters on 15 April 2026, alongside several other bilateral cooperation agreements. According to Xinhua News Agency, the agreements were

See More